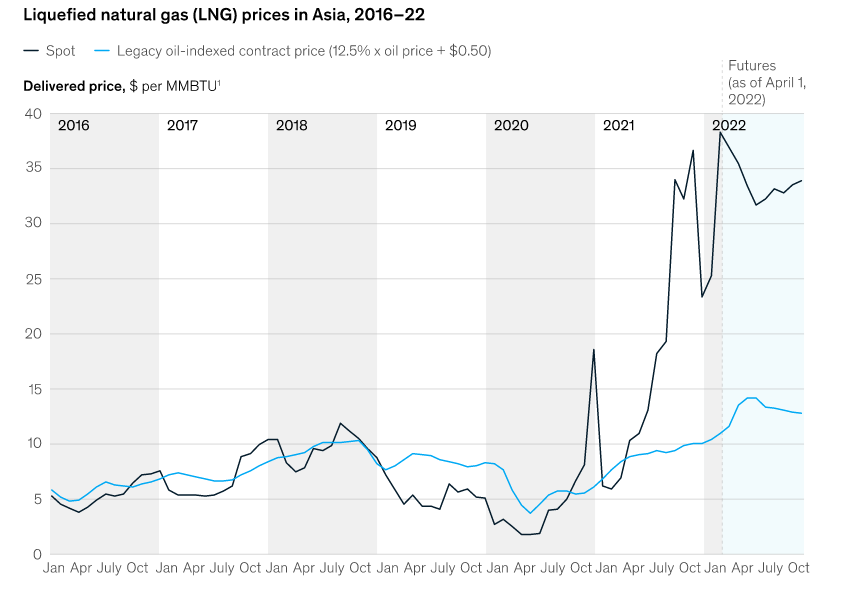

For liquefied natural gas (LNG) markets, 2021 was another unprecedented year. After the volatility, uncertainty, and record-low spot LNG prices caused by the COVID-19 pandemic in 2020, the LNG market moved in the opposite direction in 2021 (see sidebar “About the analysis”). A combination of economic recovery, European concerns about the security of supply, and operational challenges at several major liquefaction facilities sent prices to all-time highs. The average spot price for LNG in Asia in 2021 was $17.9 per metric million British thermal units (MMBTU), up 435 percent from the 2020 figure of $4.1 per MMBTU1. These factors combined to make 2021 a year of unpredictable challenges, particularly for LNG buyers.

Implications of key 2021 trends

Several key drivers help explain the unprecedented price recovery in 2021. First, operational difficulties in several projects constrained overall supply despite the recovery of US LNG projects. Second, strong Asian demand, particularly in the first nine months of the year, tightened the global LNG balance, enabling Asian buyers to fill storage. Finally, in Europe, low wind conditions and nuclear generation led to high levels of gas to power demand, which reduced the ability of European buyers to refill storage in the summer.

Given that the sustained high prices from 2021 are carrying into 2022, we are likely to see a significant downward swing if fundamentals or perceptions of market tightness change. Either of these events could be driven by a reduction in demand because of a mild end of winter or spring. However, the European market has a limited storage buffer to cope with any supply disruptions, which could result in sustained high prices.

Changes in LNG purchasing patterns

For LNG buyers, 2021 introduced stark realities. After 2019 and 2020, when spot LNG was priced at a significant discount compared with legacy oil-indexed and Henry Hub–based contracts, 2021 saw a sharp reversal (Exhibit 2). As an example, buyers with oil-indexed contracts would have paid nearly $425 million in 2021 compared with $328 million in 2020. However, one million metric tons per annum (MMTPA) in the spot market would have increased twofold over legacy oil-indexed contract prices. Indeed, over the course of the past five years, the sustained spike in spot prices in 2021 was enough to tip overall costs in favor of Henry Hub followed by oil indexation.